Authored by 720Global's Michael Lebowitz via RealInvestmentAdvice.com,

The Fed Giveth

In December 2008, at the peak of the financial crisis, the Federal Reserve (Fed) lowered the Federal Funds interest rate to zero. In taking this unprecedented step, many investment professionals assumed the Fed was out of bullets to stem the crisis.

Federal Reserve Chairman Ben Bernanke proved them wrong by introducing Quantitative Easing (QE). While the media lauded Bernanke for his creative ingenuity, the fact of the matter was that QE was already being employed in Japan on and off since 2001. Additionally, other versions of QE were used in the United States, most notably during the 1920’s. They did not call that era the roaring 20’s for nothing.

QE is often referred to as money printing because the Fed conjures U.S. dollar currency from thin air which it then uses to purchase financial securities. In this day and age, the Fed does not physically “print” new money but effectively does so electronically with a series of 1’s and 0’s. Despite the seemingly magical way money is created for the “benefit of all,” critics of QE are not so enamored with this policy tool. Maybe they understand the long history of financial hardship that has befallen nations that relied heavily on it.

After nearly a decade since the Fed first administered it, the idea of reversing QE (balance sheet reduction or monetary policy normalization) has been raised by Fed officials and Wall Street pundits. The Fed’s campaign to downplay QE and the risks of a bloated balance sheet has been effective as investors seem to have little interest in the matter. The post-crisis economy and financial markets are deeply conditioned to monetary largesse and excessive liquidity. Changes to these conditions, if they do indeed occur, will elicit “adjustments” likely in the form of severe volatility. Frequently, pivotal market events are not forecasted or appreciated until after the fact. The possibility that the Fed would embark upon a reversal of QE is one such event that will be disruptive to the artificial tranquility so enjoyed in the recent past. Despite widespread complacency, the increasing possibility of action is an important matter.

Barbie Dolls and Backhoes

At the onset of QE, many bright economists were confident that money printing would lead to inflation. Since that time, these economists have been chastised by the media for their “bad inflation call.” In fact, Ben Bernanke recently took an opportunity to pile on. At a roundtable discussion in April 2016 with current Fed Chairwoman Janet Yellen, Alan Greenspan and Paul Volcker, Bernanke stated “And many, if not all of the things people were afraid of, or some people were, I think informed people were not so afraid of, uh, were, obviously does not come to pass, I mean that’s simply a fact.”

Despite the ribbing from the media and Bernanke’s certitude, the truth of the matter is that those expressing inflationary concerns in 2008 were 100% correct. The only problem is that they failed to predict where inflation would appear. They did not appreciate at the time that those products closest to the monetary firehose would inflate.

Had the Fed literally dropped $3 trillion out of helicopters, there would have likely been a sharp increase in demand for many goods and general inflation would have risen. Conversely, if they focused $3 trillion on infrastructure projects, inflation would have shown up in construction worker wages, building supplies, and large machinery. Consider what might happen if the Federal Reserve gave every seven-year-old girl $20,000. QE focused on little girls would have resulted in soaring Barbie Doll prices. Instead, the Fed’s spigot was aimed at the large primary dealers and the financial markets. They opted to purchase previously issued U.S. Treasury securities and mortgage-backed securities (MBS) from Primary Dealers. In taking this tack, they did not give the money to little girls, construction workers or to you and me, but instead gave it to the nation’s largest banks and brokers and the financial markets in which they operate.

This surge of liquidity provided primary banks and Wall Street brokers the means to create new loans and leverage new and existing investments. In the Fed’s mind, this was critical as many markets in late 2008 and early 2009 were seizing up and in dire need of liquidity. Liquidity from QE started flowing through the markets and at first to the benefit of the most liquid securities. Over time, however, as fear receded, most asset classes started inflating, even those deeply distressed products that were the scapegoats for the crisis.

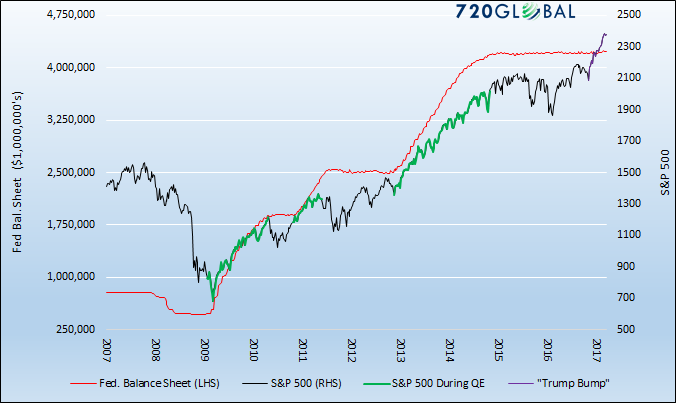

Data Courtesy: Federal Reserve and Bloomberg

The graph above shows the tight correlation between increases in the Fed’s balance sheet and stock market gains. The sustainability of the initial rally from the March 2009 lows was very much in question in both 2010 and 2011 when QE I and II ended respectively. Fortunately for investors in both instances, rumors of a new round of QE quickly became fact. Except for the recent “Trump Bump,” a rally based on optimism over Donald Trump’s economic initiatives, the market flat-lined for the better part of the post QE3 period. Since QE was first introduced, the S&P 500 has gained 1,546 points. All but 355 points were achieved during periods of QE. Of those remaining 355 points, over 80% occurred after Trump’s victory.

Inflation from QE has shown up in spades, just not in ways commonly associated with the price level of goods and services. It is occurring in investable financial assets as a direct result of QE.

The Fed Taketh

1/12/2017 “When we (Fed Funds) are at or above 100 basis points – and we are moving toward that – I think it is time to start serious consideration of first stopping reinvestment and then over a period of time unwinding the balance sheet.” Patrick Harker- Federal Reserve President Philadelphia

4/05/2017 “Provided that the economy continued to perform about as expected, most participants anticipated that gradual increases in the federal funds rate would continue and judged that a change to the Committee’s reinvestment policy would likely be appropriate later this year.” Federal Reserve FOMC meeting minutes

Based on the quotes above, serious discussions of balance sheet normalization within the Fed have begun. The Fed has raised the Federal Funds interest rate three times since December 2015 and is currently trying to convince the market they will be more aggressive going forward. As the Fed tracks further down the interest rate normalization path, debate over normalizing their balance sheet should increase exponentially. Given that money printing spurred investment leverage and generated financial asset inflation, what are the implications of a reduction in that source of liquidity? What is the risk to asset prices that have been artificially supported for several years by a severely bloated Fed balance sheet?

Summary

Frequently, the leaders of the Federal Reserve use economic jargon and big words to make their points. When one takes the time to dissect their messages surrounding QE, one is left with numerous contradictions, faulty logic, and often confusion. While the media and most investors take the bait offered by the Fed, the Fed’s logic needs to be questioned. Does it make sense and is it even coherent? If QE is such a good thing, as professed by Janet Yellen, Ben Bernanke and most other Federal Reserve Presidents why would they want to remove it? In fact, why not do more of it? 720Global will have more to say on that topic in future articles, but keep in mind that there is a reason they are hesitant to do more QE and it is deeply troubling.

Markets do not wait for events to occur. They are voting machines and constant price changes are reflective of probability changes of certain events coming to pass. We suspect that over the course of the year, the cry for policy normalization will grow louder, especially if the growth and reflation impulses show life. As it does, investors are more likely to voice concern and take appropriate action. At prior times in history, such a repricing has occurred swiftly and with vicious force, while at other times it has manifested subtly over time. Without regard for how it might happen next, it is important to keep in mind that with asset prices perched in historically high territory well above their fundamentals, investors should remain aware that QE was far and away the biggest influence driving asset price appreciation (inflation) for the last eight years.

The Fed giveth and the Fed will eventually be forced to taketh away.

You need to be a member of 12160 Social Network to add comments!

Join 12160 Social Network